- font size

-

Popular search:

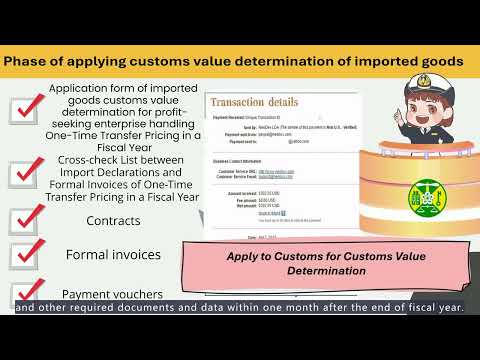

The operation of customs value determination of One-Time Transfer Pricing in a fiscal year refers to cases in which a profit-seeking enterprise makes an import declaration with controlled-transaction due to the buyer and the seller being related, and resulting in the transaction value of imported goods being unable to be determined at the time of importation and requiring to be summarized for one-time adjustment to determine its customs value in the end of a fiscal year.

For more information, please refer to the official website of Customs Administration, Ministry of Finance.

(https://web.customs.gov.tw/en/singlehtml/3510?cntId=cus16_3510_3510)